Regulation and future prospects of the Italian voluntary forestry carbon credit market

iForest - Biogeosciences and Forestry, Volume 19, Issue 3, Pages 219-225 (2026)

doi: https://doi.org/10.3832/ifor5120-019

Published: Jun 08, 2026 - Copyright © 2026 SISEF

Technical Reports

Abstract

The carbon market for the forestry sector is internationally recognized as a policy tool to reduce greenhouse gas emissions, to support afforestation and to improve forest management activities, which would not be economically viable without the sale of carbon credits. The international market is regulated by standards based on Guidelines for national greenhouse gas inventories, and in many countries, domestic markets are emerging, managed by governments whose credits can be used to meet national climate targets under the UNFCCC. In Italy, the market is currently unregulated, despite the approval of a law to establish a national registry for agriculture- and forest-based carbon credits. An analysis of the voluntary carbon credit market for the Italian forestry sector from 2011 to 2024 revealed an active market, with credit transactions priced in line with other European domestic markets. Although volumes are lower, they have been growing in recent years and peaked in the period 2021-2022. Monitoring by the Carbon Monitoring Unit highlighted critical issues and verified the impact and future prospects of the market if it is regulated by the introduction of National Guidelines and the National Registry of agriculture and forestry carbon credits.

Keywords

Carbon Credits Market, Market Governance, Forestry, Improved Forest Management, Forest Economics

Introduction

According to Wunder ([36]), the market for carbon credits generated by forestry interventions and actions falls within the category of Payments for Ecosystem Services (PES), a voluntary transaction where a well-defined ecosystem service (ES) is being “bought” by an ES buyer from an ES provider if and only if the ES provider secures ES provision (conditionality).

The forest carbon credit market is one of the main tools for combating climate change. In fact, forests contribute to climate change mitigation by absorbing about 12% of annual carbon emissions globally (net sink: +1.1 ± 0.8 Pg C year-1 - [20]), and 13% in Europe ([19]). The carbon market may provide an economic incentive to maintain or improve forest sequestration capacity by rewarding forest owners and other actors.

The core unit of this market is the “carbon credit”, which represents the removal or reduction of emissions equivalent to one ton of CO2, resulting from a carbon mitigation project that includes additional activities compared to the so-called baseline or reference scenario ([28]).

The voluntary carbon credit market for the forestry sector is active internationally following the emergence of the regulated market established by the Kyoto Protocol, with an increasing number of stakeholders and implemented projects ([8]). Transactions take place through direct bilateral agreements between buyers (companies, individuals, public and private entities, etc.) and sellers (both public and private forest owners or managers), or through intermediaries or brokers, formalised through contracts in the voluntary market, where the buyer provides financial compensation to the credit producer for the increased carbon storage or avoided emissions and the forgone profit resulting from the implementation of sustainable silvicultural practices beyond the baseline ([5], [35]).

Certified carbon credits, in accordance with Regulation (EU) 2024/3012, will help achieve the net greenhouse gas absorption target of 310 MtCO2eq set by Regulation (EU) 2018/841 on land use, land use change and forestry (LULUCF), with an absorption target for Italy of -35.8 MtCO2eq.

The Paris Agreement (Dec. 1/CP:21 par. 136) recognizes the role of carbon markets from economic, social, and environmental perspectives. Moreover, these markets assume great importance in the context of the “Green New Deal” and “Farm to Fork” strategy ([17]).

During COP29, held in Baku in 2024, it was agreed that the accreditation mechanism for Article 6.4 of the Paris Agreement will implement the new standard, Requirements for activities involving removals under the Article 6.4 mechanism (V01.0), developed by the Paris Agreement Monitoring Body, which contains requirements for activities involving removals under the Article 6.4 mechanism.

During COP30, in Belém in 2025, the Parties took note of the Baku-to-Belém Roadmap to 1.3T, a framework built in collaboration with the COP29 Presidency to scale climate finance flows to at least USD 1.3 trillion annually by 2035.

The European Union has approved Regulation (EU) 2024/3012, which establishes a certification framework for quantifying, monitoring, and verifying the Union’s carbon removals. This regulation is going to regulate the process of certifying and contribute to achieving the targets proposed by the “Fit for 55” package ([4]), presented by the European Commission on July 14, 2021, which envisages a reduction of net greenhouse gas emissions of at least 55% by 2030 compared to 1990 levels and climate neutrality in 2050.

For carbon credits to be generated from forestry activities, a certification issued by an external body adds value by confirming that the activity has been performed, the actual amount of CO2 absorbed, and converting this into corresponding saleable credits ([29]).

According to a study conducted by Sylvera ([27]), companies that buy credits reduce emissions twice as fast as those that do not. This is because the main international standards require buyers to first reduce emissions and then offset the remaining emissions.

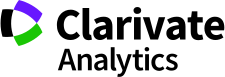

After a strong initial growth, further expansion of the voluntary carbon market has been stymied for over a decade. The outlook has changed only recently. Since 2018, the voluntary carbon market (VCM) has seen increases in both market value and volume ([5], [6], [13]). However, after two years of rapid growth, transaction volume and market value in the VCM declined in the period 2022-2024 ([7], [8] - Fig. 1). For the “Forestry and Land Use” category, transaction volume in 2024 was 37 million tonnes of CO2e (MtCO2e). Furthermore, for the second consecutive year, prices declined from their 2022 peak of $10.14/tCO2e. In 2024, credit prices remained at around $9/tCO2e, nearly double the average credit price in 2020, despite a slight 8% decline from 2023 to 2024. Due to decreases in both transaction volume and prices, the average value of the VCM decreased by 8%, to $342.5 million in 2024 ([22]).

Fig. 1 - International voluntary carbon market related to the sector Land Use, Land-Use Change and Forestry: volume and price ([22]).

Domestic markets are voluntary, national-scale markets, subject to rules set by governments that act as market regulators. Governmental bodies establish procedures and appoint regulatory agencies to conduct audits and issue certifications.

The first global voluntary carbon credits were traded in the Over The Counter (OTC) market, i.e., an unregulated market where transactions take place directly between the parties involved, followed by the development of other domestic markets worldwide. In recent years, domestic markets have emerged across Europe ([1], [2] - Tab. 1)

Tab. 1 - Main domestic markets in Europe. Italy is not included in the table because the market is not yet active ([1], [2]).

| Country | Market name | Year of market start |

Sector |

|---|---|---|---|

| United Kingdom | Woodland Carbon Code | 2011 | Forests Land use |

| Germany | Wald-Klimastandard (WKS) | 2023 | Forests |

| Spain | Registro de Huella de carbono | 2014 | Forests Land use |

| Switzerland | Max.Moore | 2015 | Forests Land use |

| Netherlands | Green Deal | 2019 | Forest Land use Renewable energies |

| France | Label Base Carbone | 2019 | Forests Land use Renewable energy |

| Sweden, Finland, and Belgium | Puro.earth | 2019 | Agriculture Durable wood products |

| Denmark | Klimaskovfunden (KSF) | 2020 | Forests Land use |

Despite these efforts and policy tools to encourage and regulate carbon markets, there remain persistent risks that inappropriate initiatives could negatively impact the sector as a whole. A distorted use of green marketing actions can lead to the risk of “greenwashing”, i.e., an unjustified appropriation of environmental virtues by organizations, aimed at creating a positive image ([32]). These regulatory and financial instruments were introduced for the purpose of regulating carbon removals, and avoiding greenwashing in response to scientific articles questioning the credibility of the market, such as those published in the journal “Science” ([33]) and in Daily press “The Guardian” ([10]) that strongly questioned the environmental integrity of credits generated by Reducing Emissions from Deforestation and Forest Degradation projects (REDD).

In both international and national markets, it is crucial to clarify market rules and verify their effectiveness in combating climate change. For Italy, it is necessary to assess the reliability of the credits sold on the market and the mechanisms that made them available for trading. It is also necessary to define the role the market could play as a policy tool to incentivize decarbonization and achieve the Paris Agreement’s reduction targets.

One of the main challenges facing the national forestry sector is the limited area of forest under continuous forest management. Evidence of this lack of management is found in the area subject to planning, which constitutes only 16.5% of the national forest area ([9]).

The costs of silvicultural activities often exceed the revenues they generate. Revenue from the sale of carbon credits can help offset the costs of sustainable forest management activities that cannot be covered by revenue or public subsidies.

Moreover, the market, which is currently free of regulatory constraints, will be regulated by national law that provides for the activation of the “Public Registry of carbon credits generated on a voluntary basis by the national Agro-Forestry Sector,” pursuant to Law no. 21 of April 2023.

This law provided for the approval of two other implementing decrees: the first was approved by the Ministry of Agriculture, Food Sovereignty and Forests (MASAF) on 15 October, in agreement with the Italian Ministry of Environment and Energy Security (MASE), and was published in the Official Gazette (see Appendix 1 in Supplementary material) on 18 November 2025, while the second is currently being drafted by MASAF.

Given that a voluntary market for forestry carbon credits is already active in Italy, the aim of this regulation is to establish a governance tool to guide this market.

Despite the existence of descriptive analysis of the Italian voluntary carbon credit market for the forestry sector, a lack of systematic scientific evaluation remains, which would investigate in an integrated manner: (i) the dynamics of price and volume formation; (ii) the governance structure and certification mechanisms that regulate market access; (iii) the degree of reliability and transparency of transactions, also in relation to recent criticism of the credibility of forest credits at international level.

This assessment is of fundamental importance because it would stimulate the economic recovery of a national sector in which the development costs of silvicultural activities exceed the value of timber and non-timber forest products without public subsidies ([18]).

The available literature focuses mainly on descriptive aspects and on annual monitoring, carried out since 2011 by the Carbon Monitoring Unit (CMU), but does not provide a critical analysis of the performance of the national market or an assessment of the potential impacts of the introduction of the public register of agroforestry credits provided for by Italian legislation.

In light of this, this study aims to answer the following research questions: (1) What are the structural characteristics, development dynamics, and methodological criticalities of the Italian voluntary forest carbon credit market? (2) What effects could the introduction of the National Public Registry have on the transparency, governance, and credibility of the market, and how could the introduction of a national standard have a positive impact on both the economic and environmental aspects of the Italian market?

By answering these questions, this study aims to make an original scientific contribution to understanding how the voluntary forest carbon credit market works in Italy and to support the development of effective governance tools.

Materials and methods

Since 2011, the CMU has been conducting annual monitoring of forestry projects related to the voluntary carbon credit market, which enables transactions involving credits generated by forestry activities ([3]). The CMU collects and analyses data on forestry projects aimed at conserving and improving ecosystem services, with a particular focus on CO2 absorption, involving Italian actors operating both nationally and internationally.

The data collected annually by the CMU has enabled the analysis and monitoring of trends in the voluntary forestry carbon credit market, with annual reports on market trends published and available for download on the CMU website (⇒ https://www.nucleomonitoraggiocarbonio.it/it/).

Data collection is based on an online survey, distributed once a year between February and April, supplemented by validation interviews and other document requests. The survey consists of four sections: (i) respondents’ personal details and role within the organization; (ii) project information (location, type of forestry operation, certification standards); (iii) information on carbon credits (prices, volumes, contract types); (iv) other ecosystem services generated by the project. The survey consists mainly of closed questions, multiple-choice questions, and open fields for additional notes and comments.

The reference population consists of Italian actors (proponents, managers, brokers, buyers) operating in the voluntary carbon credit market for the forestry sector, both in Italy and abroad. The total population cannot be observed because in an unregulated market, transactions occur through bilateral agreements between the parties. For this reason, multi-channel coverage sampling was adopted. The surveys were distributed in three ways: through the CMU website, the CMU social media channels, and by email, with the aim of obtaining a sample as representative as possible of projects carried out in Italy and abroad by Italian organizations. The invitation outlined the purpose of the study, the time frame for completion, and the conditions for data processing.

Only forestry projects carried out in Italy or abroad that involved at least one Italian actor and generated carbon sequestration during the survey period were included in the survey. All non-forestry projects, unresolvable duplicates, and incomplete or missing responses, even after interviews, were excluded.

Responses were collected digitally and, in cases where information was missing or inconsistent, online interviews or document exchanges were conducted. When multiple reports were received for the same project, priority was given to the source with the most documentary evidence to avoid duplication.

The questionnaires were distributed annually from 2012 to 2024, yielding 187 valid responses. Given that we are analyzing a voluntary, unregulated market and that questionnaire responses are voluntary, it is not possible to determine the population from which the sample is drawn. Consequently, we cannot state that the sample is representative of the population; rather, we can only observe that it is as similar to the population as possible, within these constraints.

The data contain information on: (i) price and transaction volumes; (ii) location of projects; (iii) type of forestry activities envisaged by the project; (iv) certifications used in the project; (v) use of registers for the cancellation of sold credits; (vi) additional ecosystem services generated and monitored by the project.

The data collected enabled the study of the characteristics of the national forestry VCM and allowed for a comparison with international and domestic markets to identify its strengths, weaknesses, and areas for improvement.

Respondents provided informed consent for the scientific use of the data; the published information is aggregated and anonymized.

The market’s voluntary nature and lack of regulation, which make it fragmented and unclear, imply potential self-selection biases and incomplete coverage. The absence of an official sampling frame limits the ability to estimate the absolute response rate.

To adjust for price distortions associated with the length of the data observation period, prices were deflated using an appropriate price deflator. In particular, the Harmonized Index of Consumer Prices (HICP) published by Eurostat was employed.

Results

CMU’s market monitoring confirms that the VCM in Italy is unregulated, with various public and private actors playing distinct roles: project developers, intermediaries, sellers, and buyers.

The market’s criticality lies in the fact that each of these actors uses different methods to generate, certify, and sell credits, and sometimes even operates without certification and fails to register credits in the consultable registers.

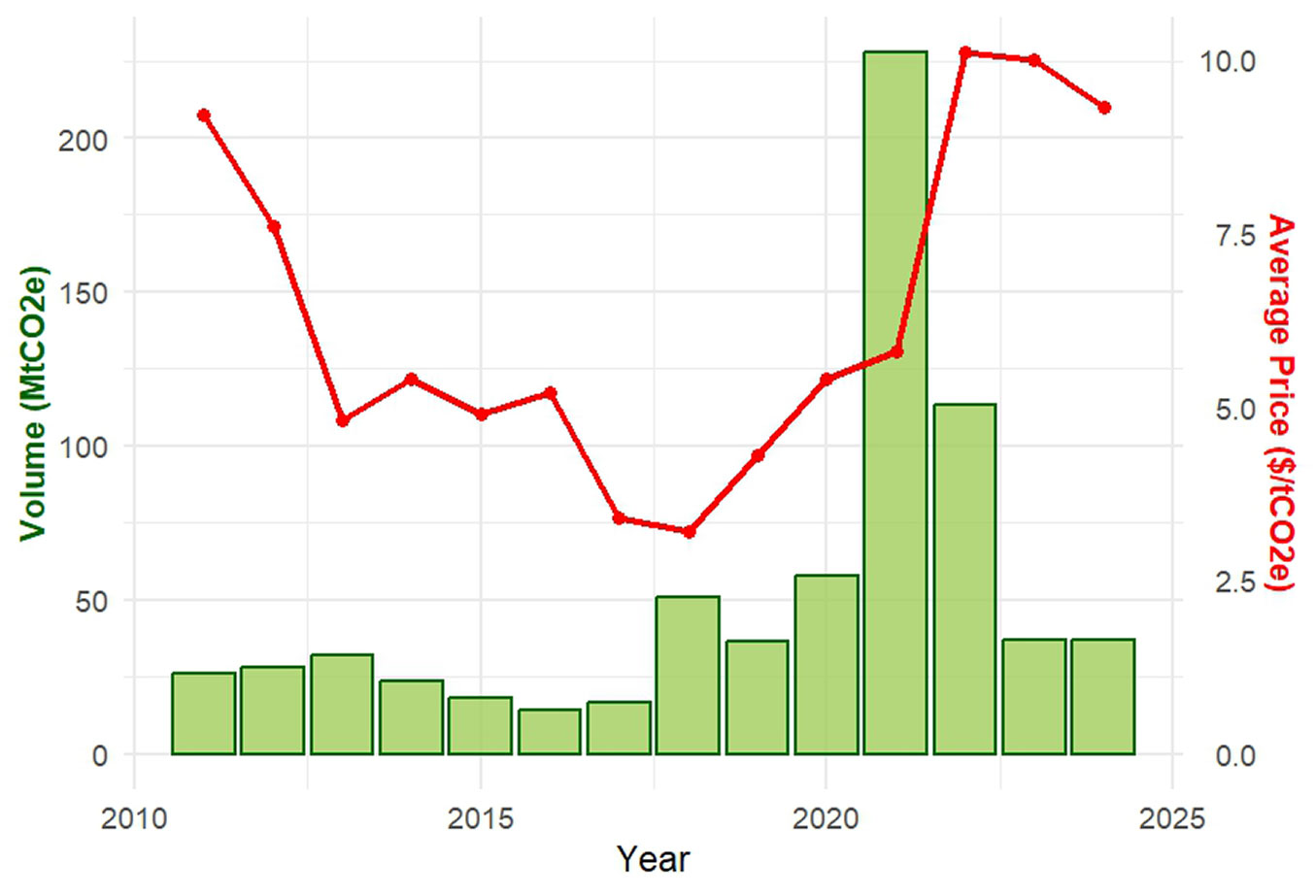

This market is characterized by significant price and volume fluctuations and is far from mature. The total volume of credits purchased from 2011 to 2024 is 3.3 million tonnes of CO2, with transactions peaking in 2021-2022, that indicates a significant market growth (Fig. 2). The price trend analysis was conducted for the period up to 2020, given the peak in tonnes sold in 2021, which may have affected price dynamics, as well as the widespread effects of the COVID-19 pandemic on the prices of goods and services in subsequent years.

Fig. 2 - Volume (tCO2) and price (€/tCO2) of carbon credit in Italy, from 2011 to 2024 ([16]).

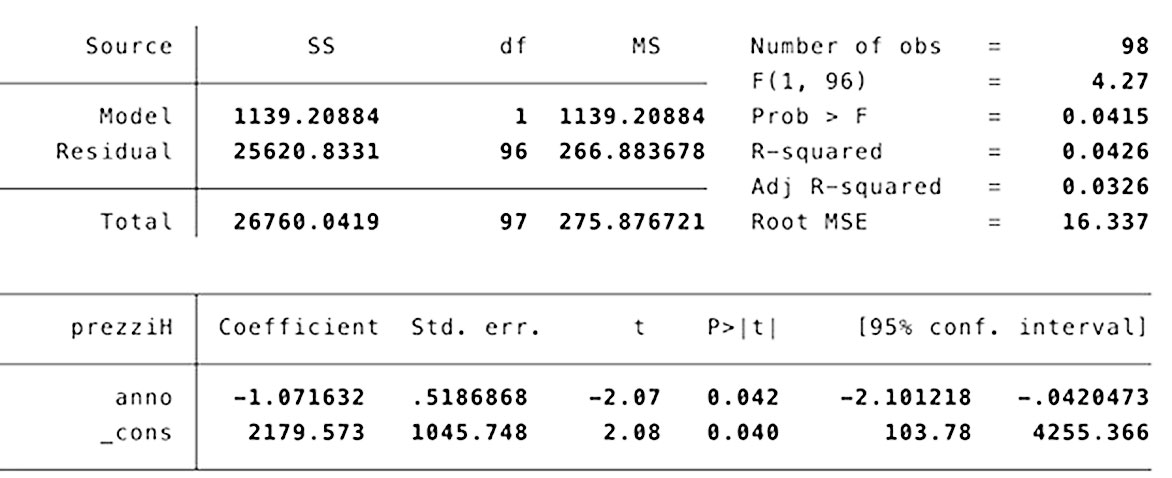

The results of the trend test indicate a negative price trend, with an estimated beta coefficient of -1.07. The effect is statistically significant, with a p-value of 0.042, and the 95% confidence intervals range from -2.10 to -0.04 (Fig. 3).

Fig. 3 - Trend test with confidence intervals for carbon credit prices over the years.

In 2022, the average price reached €28 per tonne of CO2 ([14], [15]). Over the 2023-2024 period, the market recorded a contraction in traded volumes alongside a modest decline in prices ([16]). This trend can be plausibly attributed to a natural market correction following the transaction peak observed in 2021-2022 ([15]). Overall, these developments are consistent with the prevailing dynamics of the international voluntary carbon market (Fig. 1, Fig. 2).

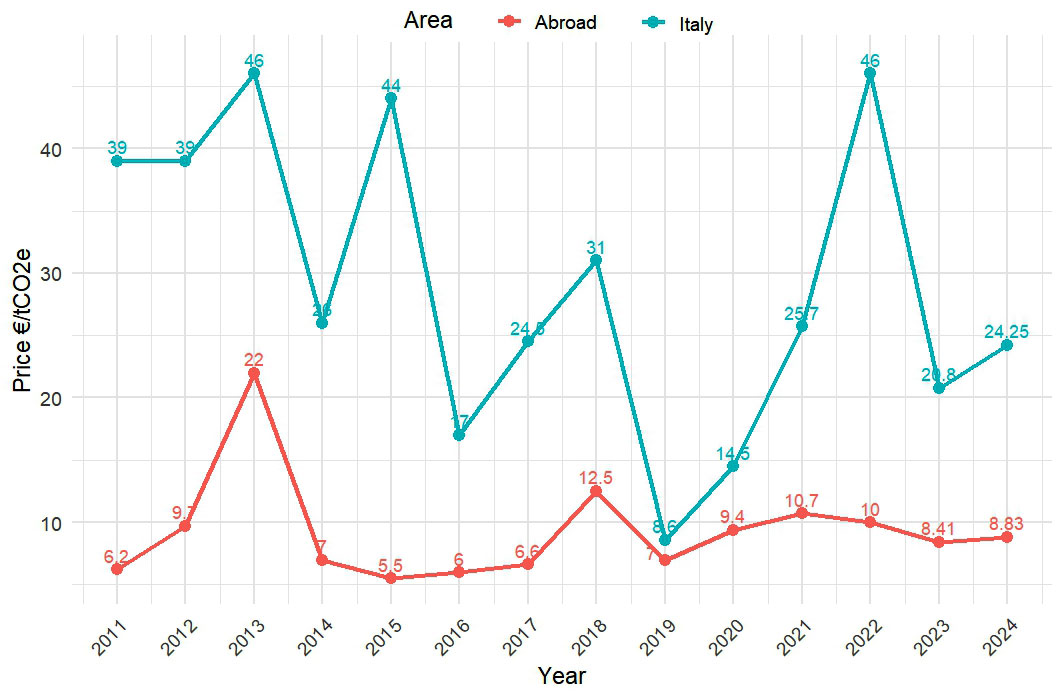

Over the last 14 years, during which the market has been monitored, buyers have preferred to purchase carbon credits generated abroad, particularly in developing countries. In the two-year period 2023-2024, only 10% of the tonnes of CO2e traded came from projects on national territory, and this percentage was even lower (5%) in the previous two-year period. The average price of credits generated in Italy between 2011 and 2024 was €29/tCO2e, whereas the average price of those generated abroad is €9.3/tCO2e (Fig. 4).

Fig. 4 - Prices per ton of CO2e generated in Italy and abroad ([16]).

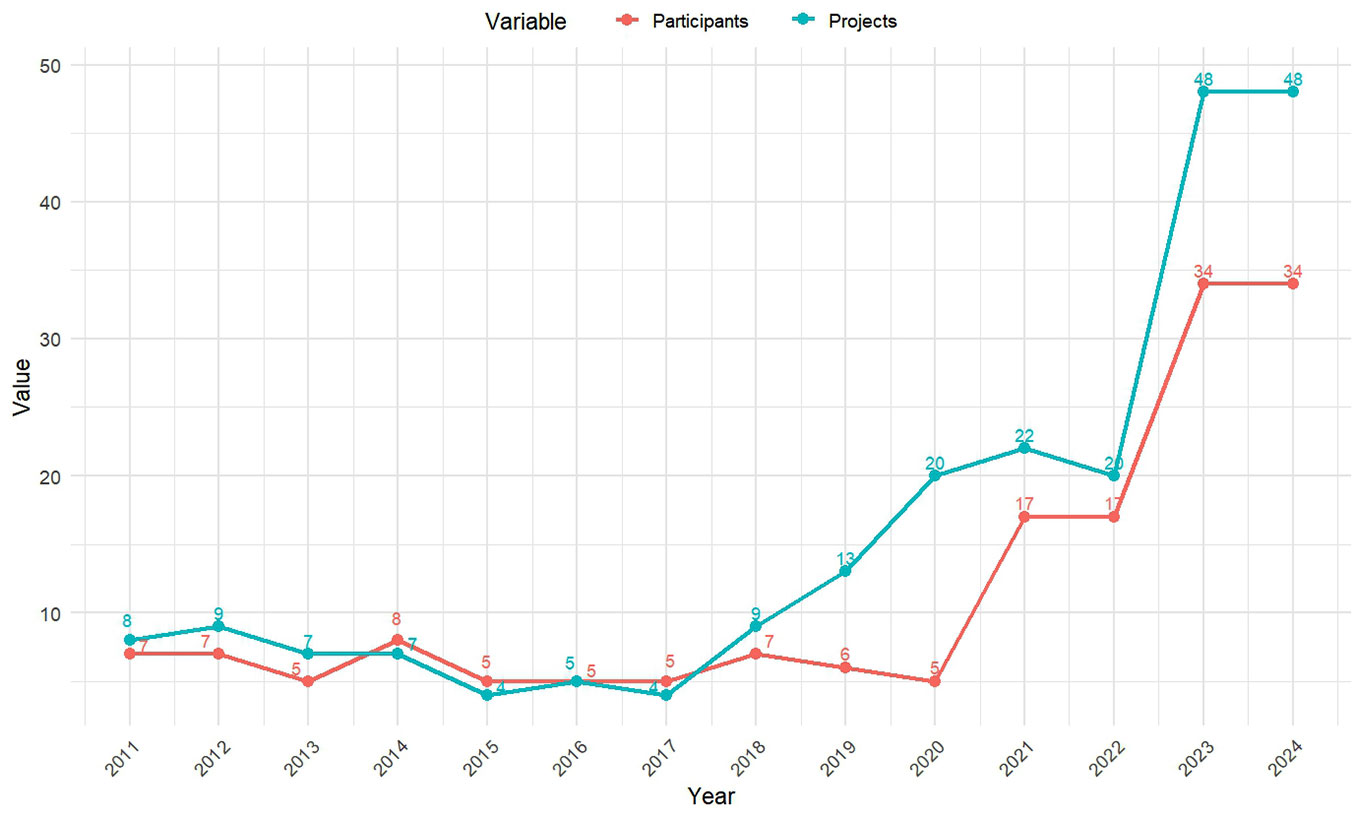

Despite issues related to credit quality and a lack of market regulation, more organizations in Italy are involved in generating and selling carbon credits. The number of projects carried out both in Italy and abroad has also increased over the last two years (Fig. 5).

Fig. 5 - Number of participants and projects implemented in the carbon credit market, from 2011 to 2024 ([16]).

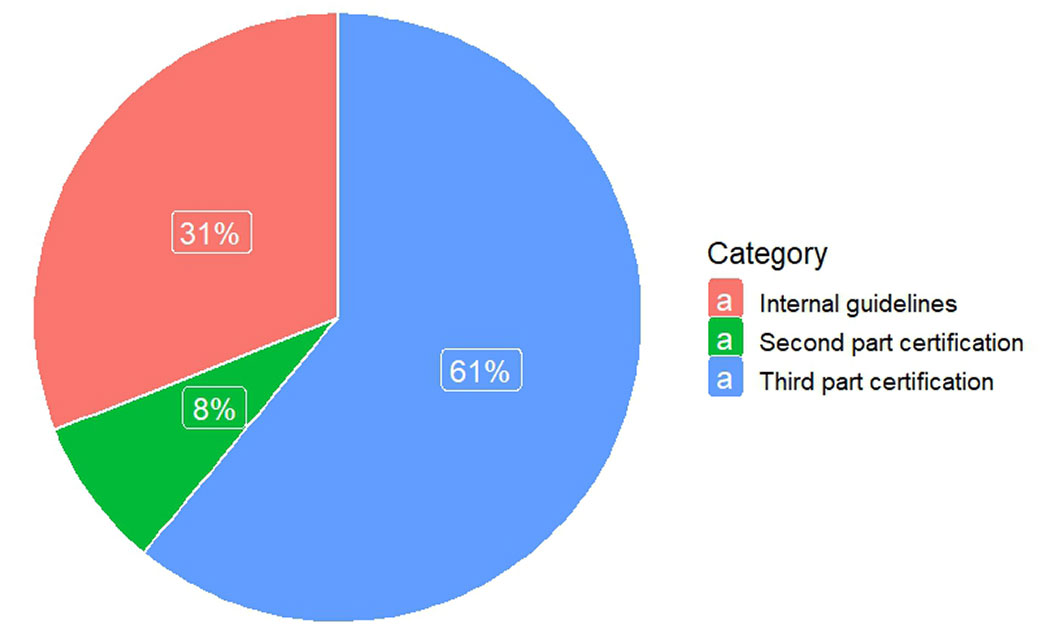

The certifications used in the market, from 2011 to 2024, can be classified into three types: (1) First-party certification: certificates issued by the brokerage agency or project developers based on internal first-party standards (declaration of conformity). (2) Second-party certification: certificates issued by external bodies based on internal second-party standards (conformity check). (3) Third-party certification: certification conducted by independent, accredited third-party bodies based on third-party standards (actual certification).

Out of 108 projects analyzed, 66 (61%) had an accredited third-party certification, 9 projects (8%) were certified by an external body that verified the correct application of a standard, and 33 projects (31%) had a declaration of conformity (Fig. 6).

Fig. 6 - Features of certification used, from 2011 to 2024.

The relationship between prices and the use of project certification was analyzed by grouping Second-party and Third-party certifications together and comparing them with First-party certifications. The latter cannot be considered genuine certifications, as they merely represent self-declarations of compliance with standards without verification by an independent external certification body. The correlation analysis reveals a slightly negative association (r = -0.3), suggesting that prices tend to be lower for projects associated with certification. However, this result should be interpreted with caution, as the observed relationship does not imply causality and may be influenced by structural and geographical factors. All non-certified projects were implemented in Italy, where prices are relatively higher, averaging €29/tCO2e, whereas projects with third-party certification are predominantly implemented in developing countries, where credit prices are substantially lower, averaging €9.3/tCO2e. Therefore, the negative correlation is likely to reflect differences in project location and market context rather than the direct effect of certification itself.

We calculated the average price of carbon credits by project type. The results indicate that afforestation projects implemented in Italy are associated with the highest average prices (€40.9/tCO2e). Carbon credits generated by GFS and agroforestry projects, implemented both in Italy and abroad, exhibit lower average prices of €16.4/tCO2e and €14.5/tCO2e, respectively. The lowest prices (7.9 €/tCO2e) are observed for carbon credits from afforestation projects in developing countries.

These findings should be interpreted with caution, as the observed price differences may be influenced by contextual factors such as project location, market maturity, regulatory environments, and cost structures, rather than by project typology alone. Consequently, the results highlight associations rather than causal relationships between project characteristics and carbon credit prices.

Discussion

The analysis of data from the voluntary carbon credit market in Italy from 2011 to 2024, reveals that forest carbon credit transactions have fluctuated significantly in price and volume (Fig. 2). These fluctuations are mainly attributed to the market’s immaturity, stemming from the absence of clear rules and guidelines, which leads to low transparency and quality in the carbon credits being sold. Investing in the unregulated market increases the risk of fraud or unfair competition, discouraging continued investment and transactions. A survey conducted by Conservation International and the We Mean Business Coalition, involving more than 500 business executives from North America and Europe, revealed that fear of greenwashing was a notable barrier for firms considering participation in voluntary carbon markets ([24]).

Italian buyers tend to prefer purchasing carbon credits generated in developing countries, where credits are produced at lower costs and are often accompanied by third-party certification. These certified credits can therefore be used by companies to obtain corporate sustainability certifications, which may help improve their ESG ratings. In contrast, forestry carbon credits generated in Italy have been less attractive in the market so far due to the lack of third-party certification. Moreover, they come with higher prices due to elevated production costs, such as carbon sequestration estimates, design costs, certification costs, credit transaction costs, and project monitoring costs.

The average selling price of forestry carbon credits generated in Italy is about three times higher than the price of credits generated abroad. However, due to high production costs, the profit for sellers remains very low. To make the market economically sustainable, it will be necessary to increase the selling price and reduce production costs.

Higher prices are also recorded in the markets of other European countries. If we consider only the domestic markets in Europe, the average is around 33 €/tCO2e ([1]), compared with an average price of forest credits in the voluntary market of 9.27 $/tCO2e ([22]).

The average prices by project type reveal that location affects prices; for example, in the case of afforestation, there is a difference of €33/tCO2e between projects carried out in Italy and those carried out in developing countries. This difference may be due to the higher costs of forestry activities in Italy.

The results presented above illustrate a market in which the low use of certification tools and registers could be influenced by the entry into force of the National Guidelines (NGLs) and the activation of the National Public Registry of Carbon Credits (see Appendix 1 in Supplementary material).

The establishment of the Registry will make the national voluntary market more transparent and credible. It is a tool to support voluntary actions, providing clear and reliable references for businesses and investors. Carbon credits are generated by projects certified by an external certification body, traded at a market-determined price, and cannot be resold to third parties or abroad. However, regulations such as the requirement to obtain third-party certification could prove burdensome, particularly for small forest owners. For this reason, the legislation also provides for group certification to offset the high costs of certification. A voluntary carbon market that aims to be effective in the fight against climate change must account for its potential risks and challenges. The market with well-defined rules, with the presence of a public body acting as guarantor and with certification issued by an independent and accredited third party, may be able to induce investors to finance projects carried out in Italy or locally, rather than subsidize projects in developing countries, which in recent years have also been criticized for their lack of effectiveness in combating climate change.

Despite its potential, VCM has faced growing criticism over concerns about greenwashing and carbon scandals. Studies have highlighted that weak regulation, lack of transparency, and fraudulent activities within VCM have led to declining trust, financial losses, and reputational risks for firms ([21], [12], [26]). The absence of uniform certification processes and inadequate monitoring mechanisms further exacerbates these issues, affecting both voluntary and compliance-based carbon markets. In addition, carbon scandals involving the overestimation of emission reductions and the sale of misleading or ineffective carbon credits have further compromised the credibility of these markets. The risk of market failure remains high, necessitating stronger verification standards, greater transparency, and better-aligned financial incentives to restore confidence in VCMs and enhance their role in climate mitigation ([26]).

In countries with active regulated domestic markets, numerous projects have been established to generate and sell very large volumes of carbon credits. For example, in the United Kingdom, the Woodland Carbon Code ([34]) has been active since 2011, and as of 31 March 2024, 621 projects have been validated, covering 34.000 hectares and sequestering 11.3 million tonnes of carbon dioxide over the entire lifetime of the projects. If we consider only Woodland Carbon Code transactions in 2024, the volume of credits sold amounts to approximately 278.000 tonnes of CO2 from forestry projects at an average price of €26.9/tCO2e. In the same year in Italy, 40.000 tonnes of CO2 were sold at an average price of €24.2/tCO2e in a free market, without a national reference standard or a national registry. The total value achieved by the two markets in 2024 is approximately €970.000 in Italy and over £7.5 million in the UK ([34]).

Another issue highlighted by the monitoring is the low use of registers in Italy. The monitoring shows that 29% of projects generate credits registered in private, non-consultable registers, 58% use public, searchable registers, and only 13% use registers created in accordance with international standards.

Using non-consultable registries or not using them is the main cause of “double selling”, i.e., selling the same carbon unit to different parties. Conversely, if the carbon credits sold are retired, they are no longer saleable to other entities, thereby increasing market transparency and reliability for buyers.

Conclusions

Despite the current lack of regulation, the voluntary carbon credit market represents an important economic sector for individuals and companies who, while seeking to offset their emissions, find an ethical commitment and ample marketing opportunities.

The regulated market, in accordance with the NGLs, will create the conditions necessary to activate an economically sustainable voluntary market. NGLs require project proponents to generate credits and submit a forest management plan. Therefore, this prerequisite could increase the area of managed forests, providing additional income to forest owners and managers. In turn, this would enhance carbon storage, improve the provision of other ecosystem services, and reduce the impacts of climate change and extreme weather events. All of this will have to take into account the baseline, which represents the carbon sink that would have occurred in the absence of the project activity, net of any negative externalities. This baseline must also consider the geographical context, including local soil, climate, and regulatory factors. However, in the Italian context, the lack of harmonized, high-quality data suitable for calculating this standardized baseline represents a significant challenge.

The regulated market will address critical issues that have emerged in the previously unregulated voluntary market, including: (i) the lack of sustained investment from credit buyers; (ii) the limited use of third-party certification and registers; (iii) the risk of greenwashing and unfair competition in the market; (iv) the shift of funding to projects in developing countries with minimal environmental value.

If buyers of carbon credits domiciled in Italy are willing to pay up to three times the price for credits generated domestically compared with those originating from developing countries - despite the frequent absence of certification for Italian credits - it is anticipated that, within a regulated framework, both the pricing and transaction volumes of domestically generated credits will experience a significant increase.

The primary objective of this study was to analyze market dynamics and explore potential future developments. Nonetheless, further research will be required to assess the actual feasibility and operational effectiveness of the proposed market framework. In particular, a comprehensive economic evaluation of forest ecosystem services such as carbon sequestration, is essential, given their substantial economic potential in mitigating climate change ([23]) and contributing to the achievement of emission reduction targets ([30]). Moreover, such services can provide valuable synergies for policymakers, enabling the attainment of policy goals at the lowest possible net economic and social cost ([25], [31]). Future analyses will therefore aim to assess the socio-economic and environmental impacts of market implementation by quantifying associated costs and benefits.

Accurate carbon price forecasts have become essential for policymakers and investors involved in related initiatives ([11]). It will be necessary to predict potential increases or decreases in credit prices by identifying key determinants from both internal and external market variables.

The European regulation on corporate sustainability statements (REG 2024/3005) and the Greenwashing Directive (2024/825) will encourage companies to be more cautious and compliant in their disclosure, demonstrating their commitment to sustainability and improving their ESG rating. Offsetting through the purchase of carbon credits helps improve the environmental look and ESG rating of companies and investment funds. However, it is essential that credits are certified by an external, accredited certification body in accordance with a standard recognized by the European Union, as stipulated in Regulation (EU) 2024/3012.

NGLs stipulate that domestic private and public investors wishing to acquire carbon credits must first commit to an emissions-reduction pathway before they can offset residual emissions through carbon credits. The NGLs are an essential governance tool for regulation, ensuring credibility and maximizing the effectiveness of Italy’s voluntary forest carbon market.

The aim of this article was to explore the voluntary carbon credit market in the forestry sector, to gain insights into market dynamics and highlight potential critical issues, including the possible introduction of a regulatory instrument such as a national registry. Our findings suggest that the methodological approach adopted in this study may not be sufficient to fully identify the underlying drivers of price variation. In particular, a more comprehensive analytical framework is required to account for the simultaneous interaction of multiple variables influencing carbon credit prices. Similarly, regarding the assessment of the potential impacts of introducing the registry, our results indicate that a dedicated cost-benefit analysis would be more appropriate for adequately addressing this research question.

Abbreviations

The following abbreviations are used in this paper:

- IPCC: Intergovernmental Panel on Climate Change

- UNFCCC: United Nations Framework Convention on Climate Change

- ES: Ecosystem service

- PES: Payments for Ecosystem Services

- LULUCF: land use, land use change, and forestry

- VCM: Voluntary carbon market

- OTC; Over The Counter

- REDD: Reducing Emissions from Deforestation and Forest Degradation projects

- CMU: Carbon Monitoring Unit

- NGLs: National Guidelines

- HWP: harvested wood products

- ECB: External Certifying Body

- FPD: Forestry Project Document

- CREA: Council for Agricultural Research and Economics

Author Contributions

Conceptualization, S.M. and R.R.; methodology, S.M. and T.G.; validation, S.M., R.R., and T.G.; formal analysis, S.M. and T.G.; investigation, S.M. and T.G.; writing - original draft preparation, S.M. and T.G.; writing - review and editing, S.M., R.R., and T.G.; visualization, S.M. and T.G.; supervision, S.M. and R.R.; project administration, S.M.; funding acquisition, S.M. and R.R. All authors have read and agreed to the published version of the manuscript.

Funding

This work was funded by a dedicated research initiative by the Council for Agricultural Research and Analysis of Agricultural Economics (CREA), initially funded by the 2014-2020 National Rural Network project and now by the 2025-2029 CAP Network Project.

References

Gscholar

Gscholar

Gscholar

Gscholar

Gscholar

Gscholar

Gscholar

Authors’ Info

Authors’ Affiliation

Teresa Grassi 0009-0005-5981-9656

Raoul Romano 0000-0003-2158-5266

Council for Agricultural Research and Economics - Policies and Bioeconomy Research Center, Rome (Italy)

Corresponding author

Paper Info

Citation

Maluccio S, Grassi T, Romano R (2026). Regulation and future prospects of the Italian voluntary forestry carbon credit market. iForest 19: 219-225. - doi: 10.3832/ifor5120-019

Academic Editor

Marco Borghetti

Paper history

Received: Dec 19, 2025

Accepted: Apr 05, 2026

First online: Jun 08, 2026

Publication Date: Jun 30, 2026

Publication Time: 2.13 months

Copyright Information

© SISEF - The Italian Society of Silviculture and Forest Ecology 2026

Open Access

This article is distributed under the terms of the Creative Commons Attribution-Non Commercial 4.0 International (https://creativecommons.org/licenses/by-nc/4.0/), which permits unrestricted use, distribution, and reproduction in any medium, provided you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license, and indicate if changes were made.

Web Metrics

Breakdown by View Type

Article Usage

Total Article Views: 1358

(from publication date up to now)

Breakdown by View Type

HTML Page Views: 304

Abstract Page Views: 659

PDF Downloads: 297

Citation/Reference Downloads: 0

XML Downloads: 98

Web Metrics

Days since publication: 62

Overall contacts: 1358

Avg. contacts per week: 153.32

Article Citations

Article citations are based on data periodically collected from the Clarivate Web of Science web site

(last update: Jul 2026)

(No citations were found up to date. Please come back later)

Publication Metrics

by Dimensions ©

Articles citing this article

List of the papers citing this article based on CrossRef Cited-by.

Related Contents

iForest Similar Articles

Research Articles

Voluntary carbon credits from improved forest management: policy guidelines and case study

vol. 11, pp. 1-10 (online: 09 January 2018)

Editorials

Change is in the air: future challenges for applied forest research

vol. 2, pp. 56-58 (online: 18 March 2009)

Research Articles

Shifting to a holistic approach in national wildfire management policies: the Italian case

vol. 18, pp. 163-175 (online: 01 July 2025)

Research Articles

Integrating forest-based industry and forest resource modeling

vol. 9, pp. 743-750 (online: 12 August 2016)

Research Articles

Approaches to classifying and restoring degraded tropical forests for the anticipated REDD+ climate change mitigation mechanism

vol. 4, pp. 1-6 (online: 27 January 2011)

Research Articles

Forest management with carbon scenarios in the central region of Mexico

vol. 14, pp. 413-420 (online: 15 September 2021)

Review Papers

Carbon neutrality of forest biomass for bioenergy: a scoping review

vol. 16, pp. 70-77 (online: 05 March 2023)

Research Articles

Seeing, believing, acting: climate change attitudes and adaptation of Hungarian forest managers

vol. 15, pp. 509-518 (online: 14 December 2022)

Review Papers

Comparative assessment for biogenic carbon accounting methods in carbon footprint of products: a review study for construction materials based on forest products

vol. 10, pp. 815-823 (online: 25 September 2017)

Research Articles

An assessment of climate change impacts on the tropical forests of Central America using the Holdridge Life Zone (HLZ) land classification system

vol. 6, pp. 183-189 (online: 08 May 2013)

iForest Database Search

Search By Author

Search By Keyword

Google Scholar Search

Citing Articles

Search By Author

Search By Keywords

PubMed Search

Search By Author

Search By Keyword